Most traders believe edge is simply a high win rate. That assumption destroys more trading systems than market volatility.

A strategy can win only 35% of its trades and remain highly profitable. Another can achieve an 80% win rate while steadily losing capital.

The difference is edge.

The Misunderstanding Behind Trading Edge

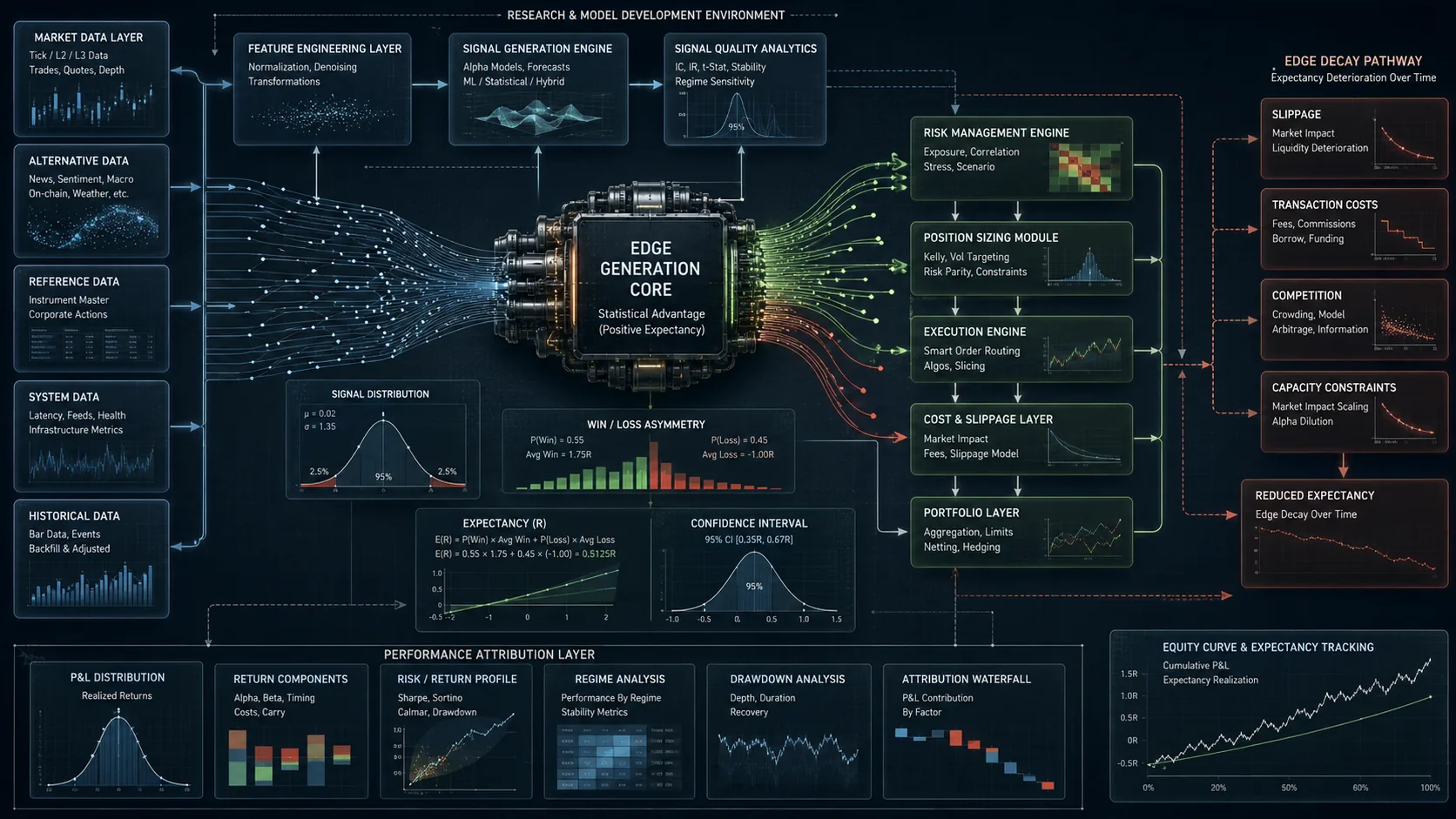

In a quantitative trading system, edge is a measurable statistical advantage that produces a positive expected outcome across a sufficiently large sample of trades.

Edge is not a signal. It is not an indicator. It is not a prediction.

Edge is a property of the system's output distribution.

Viewing Edge as a System

Every quant strategy can be modeled as:

Inputs → Signal Generation → Execution Layer → PnL Distribution

Many practitioners mistakenly search for edge inside entry signals. In production environments, edge exists within the behavior of the complete system.

This distinction becomes critical once execution costs and operational constraints appear.

How Is Edge Calculated?

The most common approach uses mathematical expectancy.

Edge = (Win Rate × Average Win) − (Loss Rate × Average Loss)

Example:

- Win Rate = 45%

- Average Win = 3%

- Loss Rate = 55%

- Average Loss = 1%

Result:

Edge = (0.45 × 3) − (0.55 × 1)

Edge = 0.8%

The expected value of every trade is positive. That small number becomes significant when compounded across thousands of executions.

Why Edge Matters More Than Win Rate

| System | Win Rate | Average Win | Average Loss | Edge |

|---|---|---|---|---|

| A | 80% | 1% | 5% | Negative |

| B | 40% | 4% | 1% | Positive |

Markets do not reward winning frequency. They reward positive expectancy.

The distribution of outcomes matters more than the count of successful trades.

Where Does Edge Come From?

Quantitative trading systems typically derive edge from one or more of the following sources:

- Behavioral market inefficiencies

- Information delays

- Market microstructure effects

- Risk premia

- Persistent statistical relationships

- Execution advantages

No edge is permanent.

Every edge competes against capital, technology, and market adaptation.

Edge Decay: The Production Reality

One of the most overlooked realities in quantitative trading is edge decay.

As capital scales:

- Slippage increases.

- Competition intensifies.

- Market behavior adapts.

- Execution costs rise.

The original advantage begins to erode.

A strategy showing 2% expectancy in backtests may deliver only 0.2% after deployment.

Common Edge Measurement Failures

Ignoring Transaction Costs

Commissions, spreads, and slippage directly consume edge.

Many apparently profitable systems disappear once realistic costs are applied.

Overfitting Historical Data

A strategy may appear to possess edge only because it has been optimized around historical noise.

Production deployment quickly exposes the illusion.

Insufficient Sample Size

Twenty profitable trades do not prove statistical advantage.

The observed results may simply be randomness.

Survivorship Bias

Analysts often study successful strategies while ignoring the thousands that failed.

This creates a distorted understanding of what constitutes genuine edge.

The Relationship Between Edge and Risk Management

Positive expectancy alone is not enough.

An edge can still lead to ruin if position sizing and risk controls are poorly designed.

Professional trading architectures typically combine:

Edge Engine + Risk Engine + Execution Engine

These components must function as a single integrated system.

A Practical Quant System Example

Consider a mean-reversion strategy deployed in cryptocurrency markets.

Backtest metrics:

- Expectancy = 1.4%

- Sharpe Ratio = 2.1

- Maximum Drawdown = 9%

After production deployment:

- Commissions appear.

- Slippage emerges.

- Network latency affects execution.

- Liquidity constraints become visible.

Expectancy drops to 0.4%.

The backtest measured theoretical edge. The live environment measured operational edge.

The Core Trade-Off: Edge vs Scalability

The most important architectural tension in quantitative trading is not profitability.

It is the balance between edge strength and edge scalability.

Many powerful edges have limited capacity. Increasing capital eventually destroys the opportunity itself.

Weaker but more scalable edges often outperform stronger edges at portfolio scale.

System design is not about maximizing returns. It is about maximizing sustainable returns under real-world constraints.

Key Takeaways

- Edge is a measurable statistical advantage.

- Win rate alone does not define profitability.

- Expectancy is the most common edge measurement framework.

- Execution costs must be included in every calculation.

- Edge naturally decays over time.

- Scalability constraints are often more important than raw profitability.

- Professional systems protect, monitor, and continuously validate edge.

FAQ

Is edge the same as alpha?

No. Alpha usually refers to excess return relative to a benchmark, while edge refers to any exploitable statistical advantage.

What is a good trading edge?

There is no universal threshold. Capacity, execution costs, turnover, and risk profile all influence what constitutes a meaningful edge.

Can a high win rate guarantee edge?

No. A system with a high win rate can still have negative expectancy if losses are sufficiently large.

Does every edge eventually decay?

In most cases, yes. Market participants adapt and competitive pressure reduces exploitable inefficiencies over time.

What is the most practical way to evaluate edge?

Measure expectancy after incorporating commissions, spread, slippage, liquidity constraints, and execution realities.

Comments (0)

You need to log in to post a comment.

Login / Sign up